In the fast-paced world of real estate investing, agility is a competitive advantage. Traditional mortgages can slow down investors with requests for personal tax returns, pay stubs, and strict debt-to-income (DTI) limits. DSCR (Debt Service Coverage Ratio) loans flip the script entirely: lenders care about the property’s cash flow, not your personal paycheck.

If you are looking to scale a portfolio, here is a breakdown of the benefits and mechanics of DSCR loans, touching on the 10 critical elements of this financing strategy.

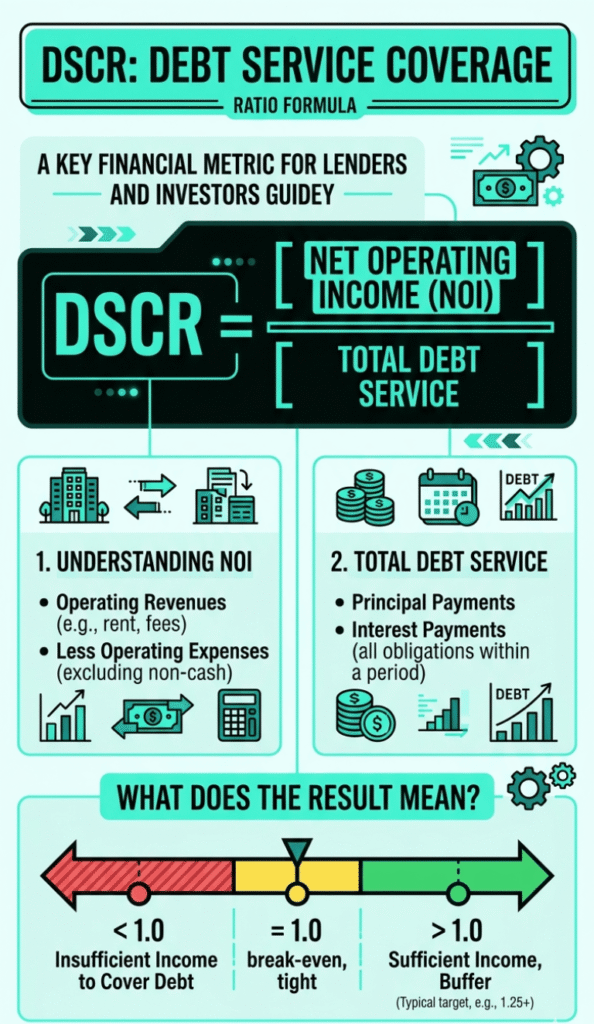

The Engine of the Loan: Cash Flow Over Income

1. The Calculation Formula

Instead of analyzing your personal expenses, lenders use a straightforward mathematical equation to determine if the property can pay for itself.

DSCR = Gross Monthly Rent / PITIA

(Note: PITIA stands for Principal, Interest, Taxes, Insurance, and HOA dues).

2. Minimum DSCR Requirements

Lenders use this ratio to gauge risk. The higher the number, the safer the investment.

- The 1.25 Sweet Spot: If your ratio is 1.25, the property generates 25% more income than its monthly debt. Hitting this tier usually unlocks the best interest rates and maximum leverage.

- The 1.0 Baseline: A 1.0 ratio means the property exactly breaks even.

- Sub-1.0 and “No-Ratio”: Some lenders will accept a ratio of 0.75 or lower, meaning the property operates at a slight loss. However, you will need to offset this risk with a larger down payment and/or cash reserves.

3. No Income Verification (The Biggest Perk)

Because the loan is entirely secured by the property’s performance, there is zero personal income verification. You do not need to provide W-2s, 1099s, or tax returns. This is a massive benefit for self-employed investors with heavy business write-offs, or those who want to protect their personal DTI for a primary home purchase.

The Financial Blueprint: Rates, Down Payments, and Credit

4. DSCR vs. Conventional Interest Rates

Because lenders take on slightly more risk by ignoring your personal income, DSCR loans price slightly higher. However, the trade-off for scalability can be worth the spread.

5. Down Payment & LTV Limits

You cannot buy a DSCR property without a down payment. Lenders require you to have skin in the game, and not a low amount like on a FHA loan.

6. Credit Score Minimums

While your income doesn’t matter, your track record of paying debts still does.

- DSCR still has relaxed credit requirements. You don’t need a 700 credit score.

- To get the best possible terms and maximum leverage, lenders want to see higher credit scores.

Flexibility and Speed for Modern Investors

7. LLC and Entity Vesting

Conventional loans are usually closed in your personal name, which isn’t ideal for liability. DSCR loans are built for business. You can close directly in the name of an LLC or corporation, giving you better asset protection and cleaner accounting.

8. Short-Term Rental (STR) Eligibility

Financing a vacation rental used to be incredibly difficult. Today, it is a standard DSCR product. We can use AirDNA data or alternative market rent analyses to project the income of a short-term rental, allowing you to finance an Airbnb just as easily as a 12-month lease.

9. Closing Speed

Removing personal tax returns from the equation means there is no weeks-long manual underwriting process. If your appraisal and title work clear quickly, the closing happens rather quickly.

The Trade-Off

10. Prepayment Penalty Structures

Because these are business-purpose loans, lenders want to hedge their long-term returns. They may attach a prepayment penalty if you sell or refinance too early.

- The Standard Structure: A common format is a “5/4/3/2/1” step-down penalty. This means you pay a penalty equal to 5% of the loan balance if you sell or refinance in Year 1, 4% in Year 2, and so on until it drops off completely.

The Math in Action

Let’s look at how a lender evaluates a potential deal to see if it qualifies for top-tier financing. This is strictly for educational purposes:

- Purchase Price: $400,000

- Down Payment: 25% ($100,000)

- Loan Amount: $300,000

- Monthly PITIA (Mortgage, Taxes, Insurance): $2,350

- Projected Monthly Rent: $3,100

DSCR = $3,100 / $2,350

- Result: 1.31

Because 1.31 is comfortably above the 1.25 threshold, this property generates excellent cash flow. It can be considered a highly attractive asset and should easily qualify for the most competitive DSCR rates on the market.

Do you have a speculative property that you would like a DSCR calculated for?